"Brazil is cheap." Sure. So what?

A country priced like its flip-flops.

Brazil is cheap. You’ve heard that before.

Three different headlines, the same thesis. Morgan Stanley, Benchimol, dozens of analysts repeating the formula. And the Brazilian investor, tired of losing money, wants to believe.

The numbers that follow come from Bloomberg, MSCI, and the IMF. None of them are opinions. They cover six dimensions of the Brazilian economy that are deteriorating at the same time and that, taken together, tell a story most of the market would rather ignore.

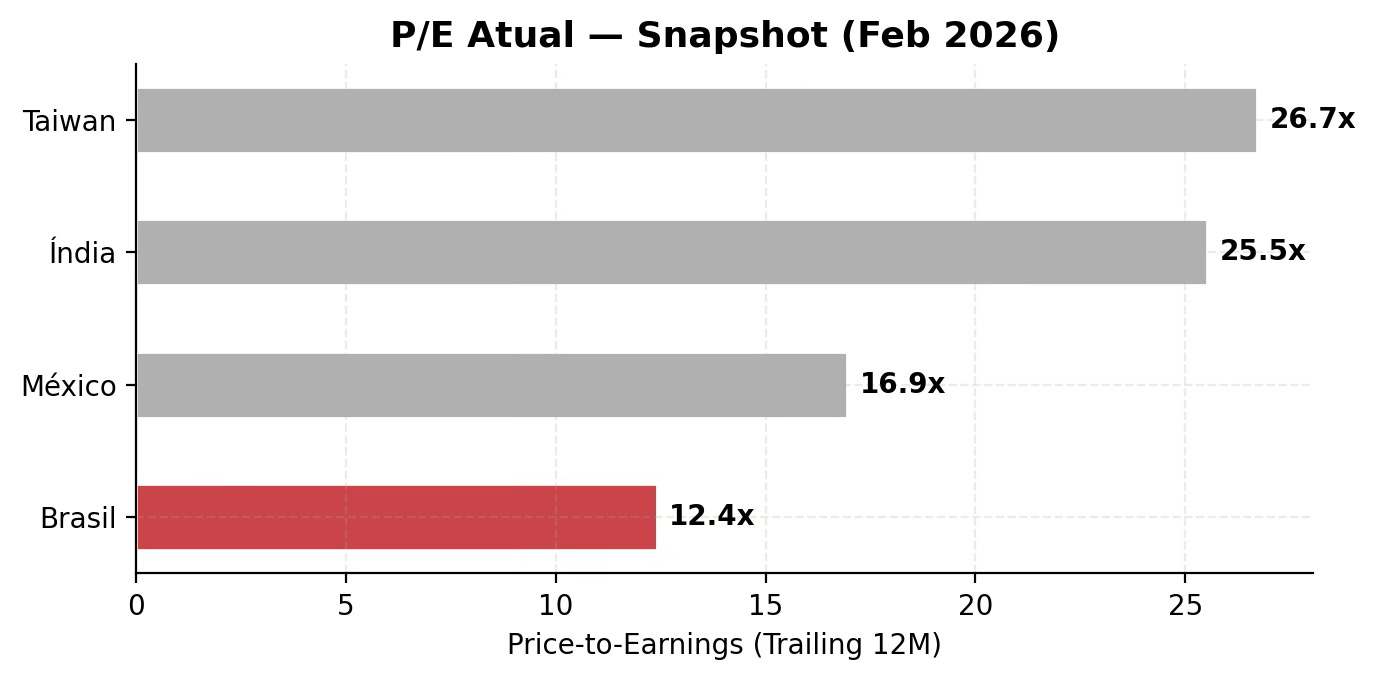

1. “Cheap” for 16 years. An opportunity? I don’t think so.

Brazil’s P/E (price-to-earnings) ratio sits at 12.4x. India is at 25.5x. Taiwan, 26.7x. Mexico, 16.9x.

Most emerging markets don’t trade at P/Es this low. Seems obvious, then: let’s buy Brazil. Big institutional investors must be seeing this discount and piling in, right?

Maybe. But if that’s true, why hasn’t this “distortion” corrected itself in the past 16 years?

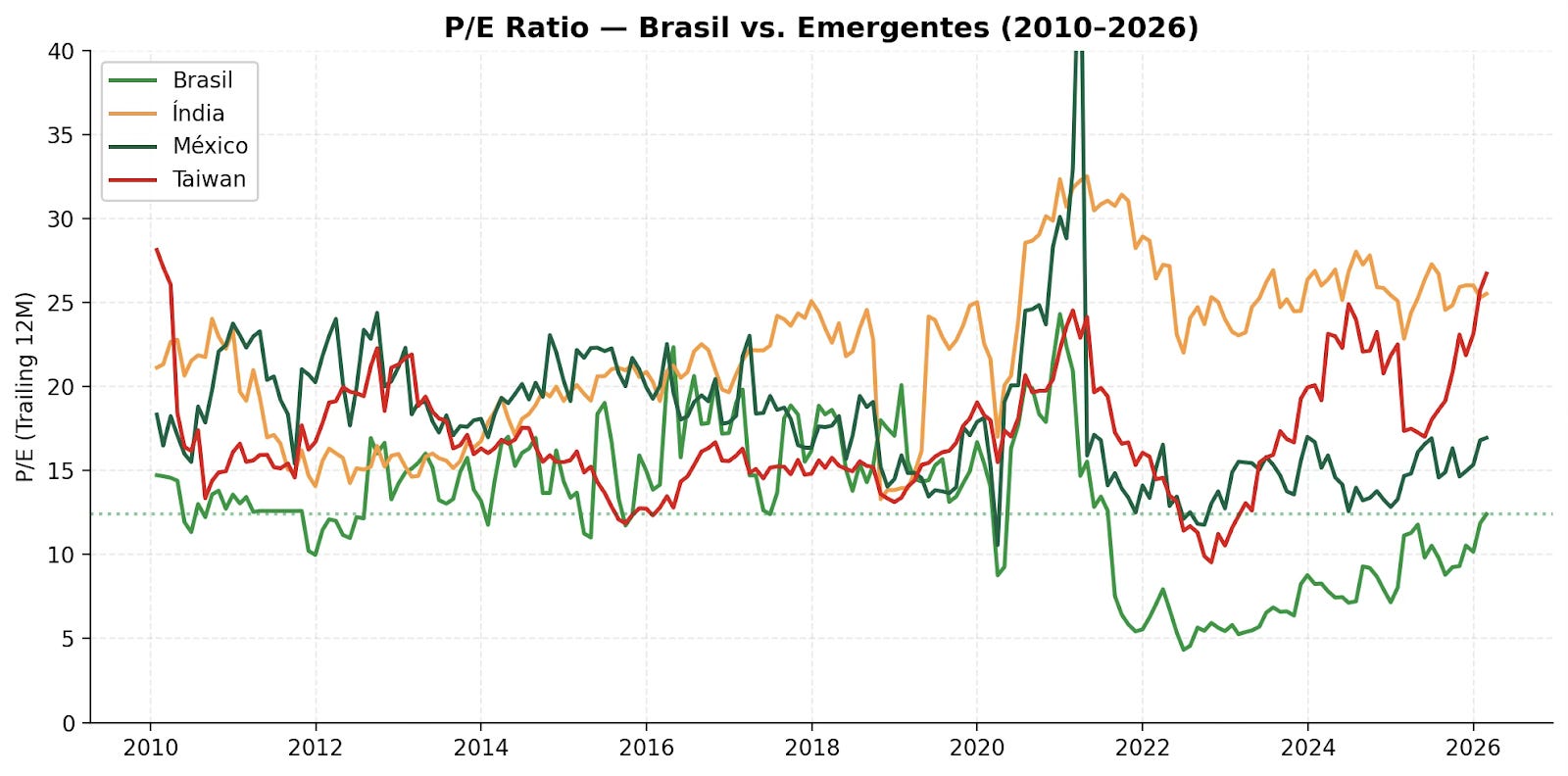

The green line is Brazil. Always at the bottom. While India, Taiwan, and Mexico oscillate between 15x and 30x, Brazil stays trapped in the 7x to 14x range. The market hasn’t been making a pricing mistake for a decade and a half. It’s pricing in real risks.

And companies are about to face even more pressure. The tax reform being phased in between 2026 and 2033 will squeeze corporate margins further. The combined tax rate exceeds 28%. Interest on equity, social contributions, dividends: everything went up. Brazil, which already fails to attract enough capital despite being one of the cheapest markets, will become less attractive as margins shrink.

2. The Real appreciated in 2025. Wow! (Other appreciated more)

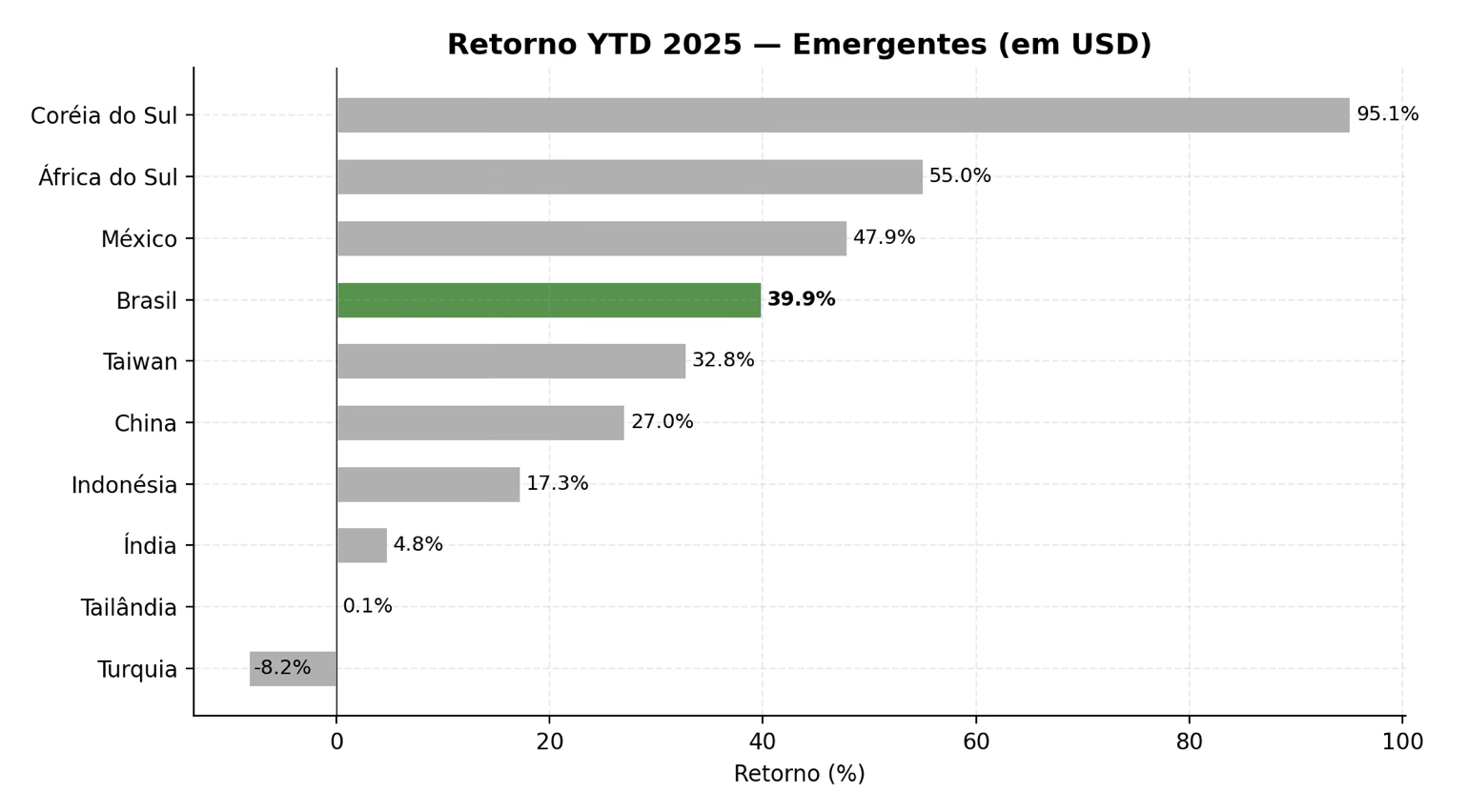

Brazil returned 39.9% in dollar terms in 2025. The exchange rate went from R$6.30 to R$5.11. Looks good, until you look around.

South Korea returned 95.1%. South Africa, 55%. Mexico, 47.9%. Brazil shows up in green in the middle of the chart, above average but below nearly every relevant peer.

This wasn’t Brazil’s doing. Investors pulled money out of the US and spread it across emerging markets. China led the pack: DeepSeek added $1.3 trillion to Chinese equities in a single month. Brazil rode the wave. And still came in behind.

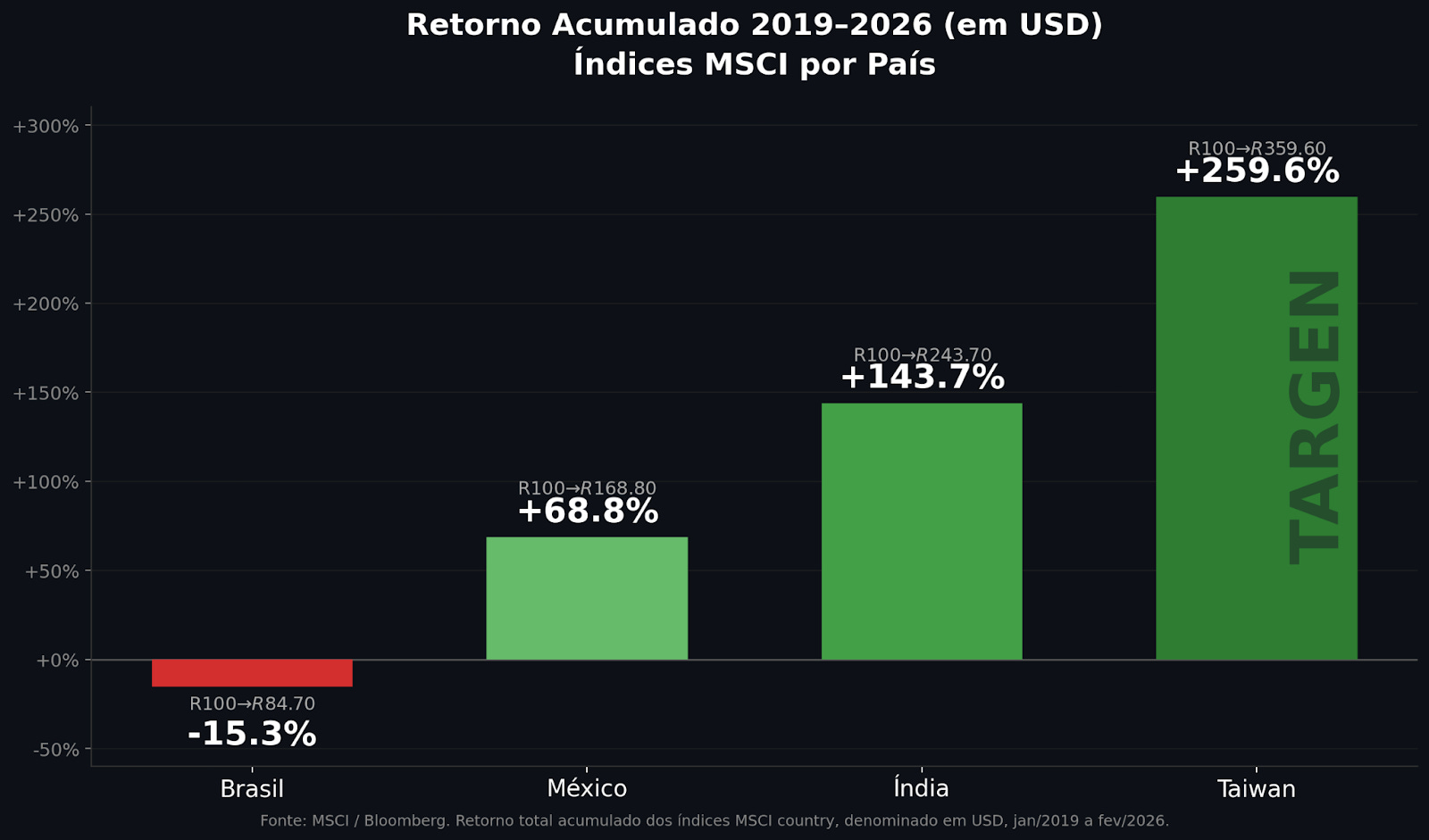

Over the long term, the picture gets worse.

From 2019 to 2026, seven years, Brazil posted a negative return: −15.3%. Someone who invested 100 in the Brazilian stock market in 2019 now has 84.70. The same 100 in Taiwan would be worth 359. That’s the direct effect of the Real’s depreciation.

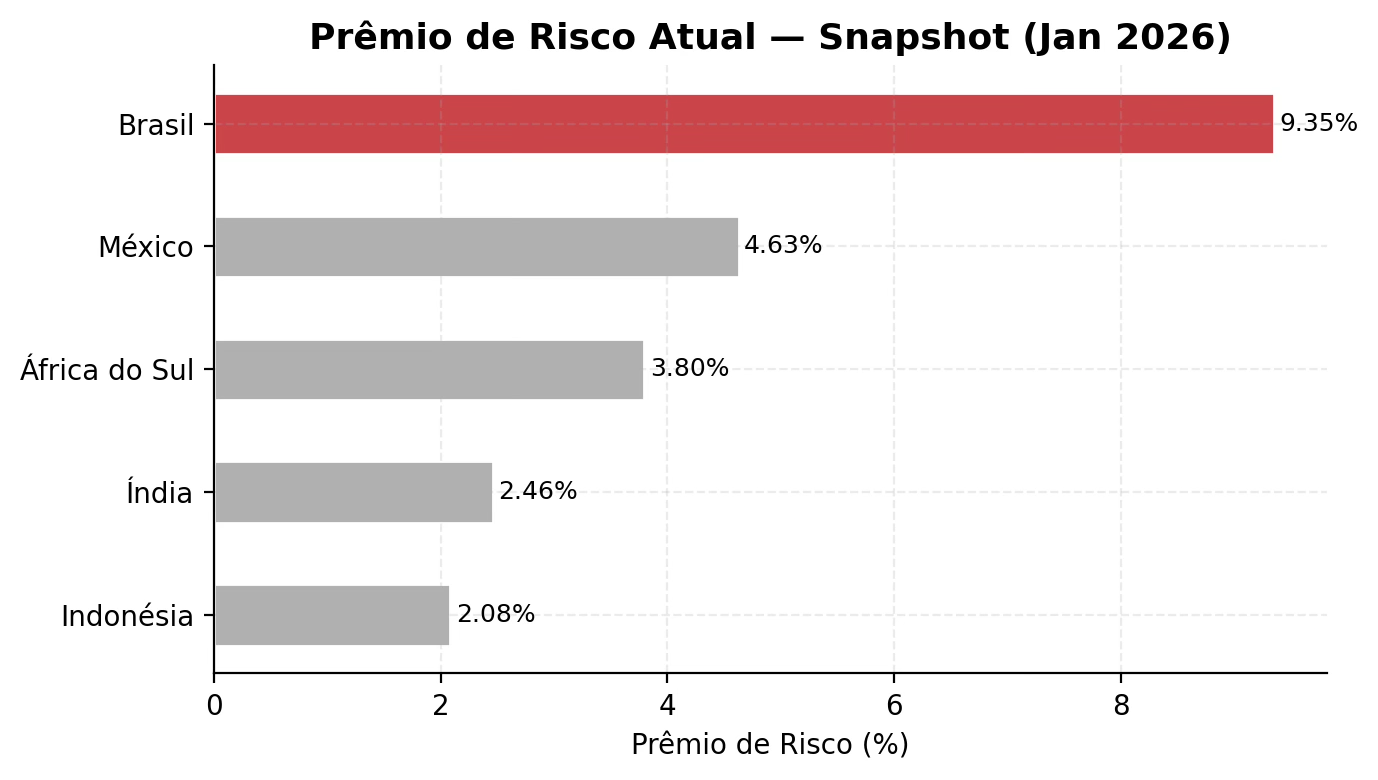

3. The market charges double to accept Brazilian risk

When you invest, there’s a safe option: US Treasuries, which currently pay between 3.5% and 3.75%. Anything riskier needs to pay a premium above that. This difference is the equity risk premium.

Mexico pays 4.63% above the risk-free rate. India, 2.46%. South Africa, 3.8%. Brazil: 9.35%. Double Mexico’s. Nearly four times India’s.

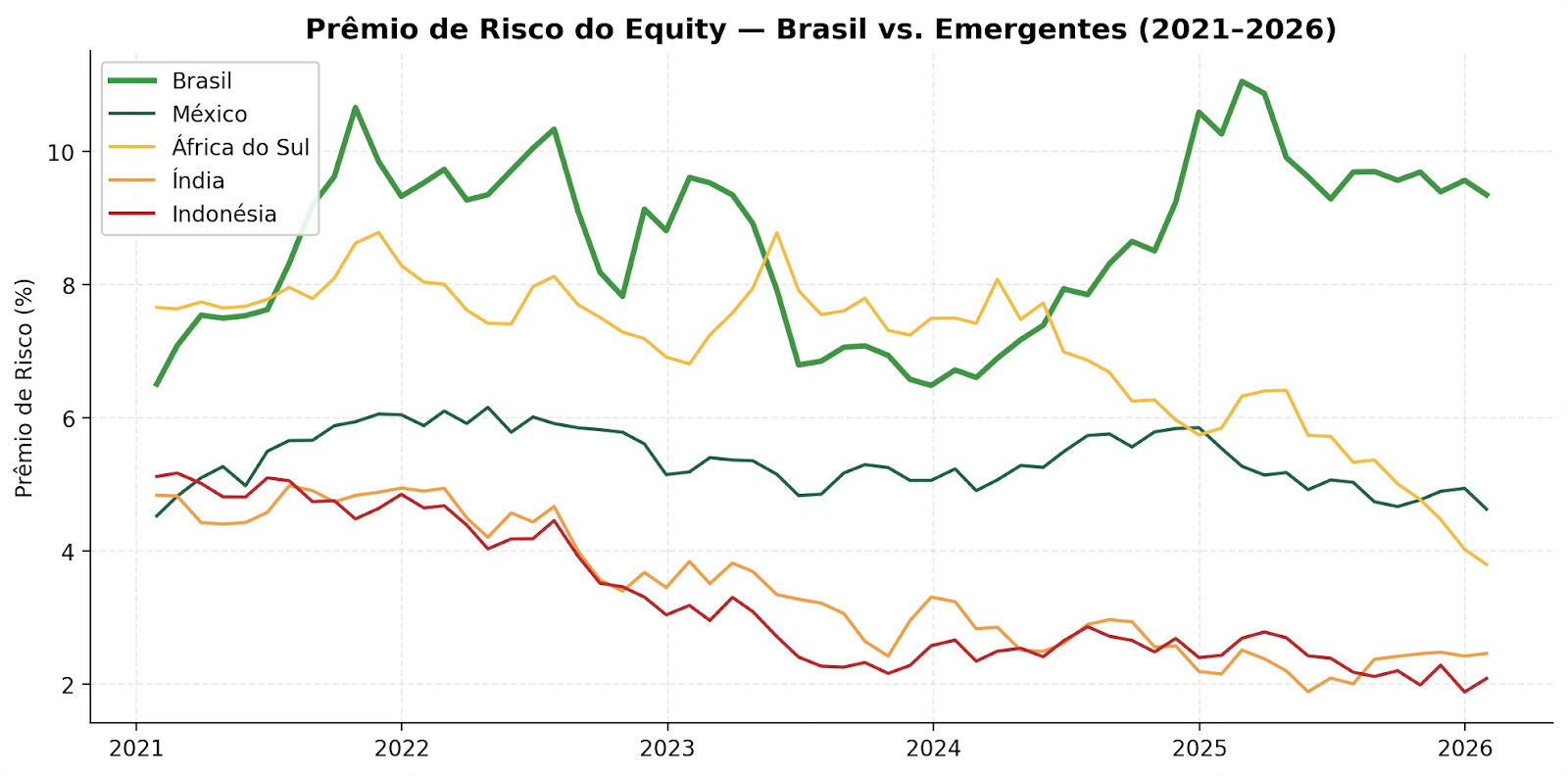

And the gap keeps widening.

The green line, far above the rest, is Brazil. While other emerging markets converge into a 2% to 5% range, Brazil’s premium has climbed steadily since 2023 and now sits near 10%.

Brazil’s public debt is heading toward 95% of GDP by 2026 and 99% by 2030. Mandatory spending accounts for 92% of the federal budget. This isn’t the market overreacting. These are the numbers.

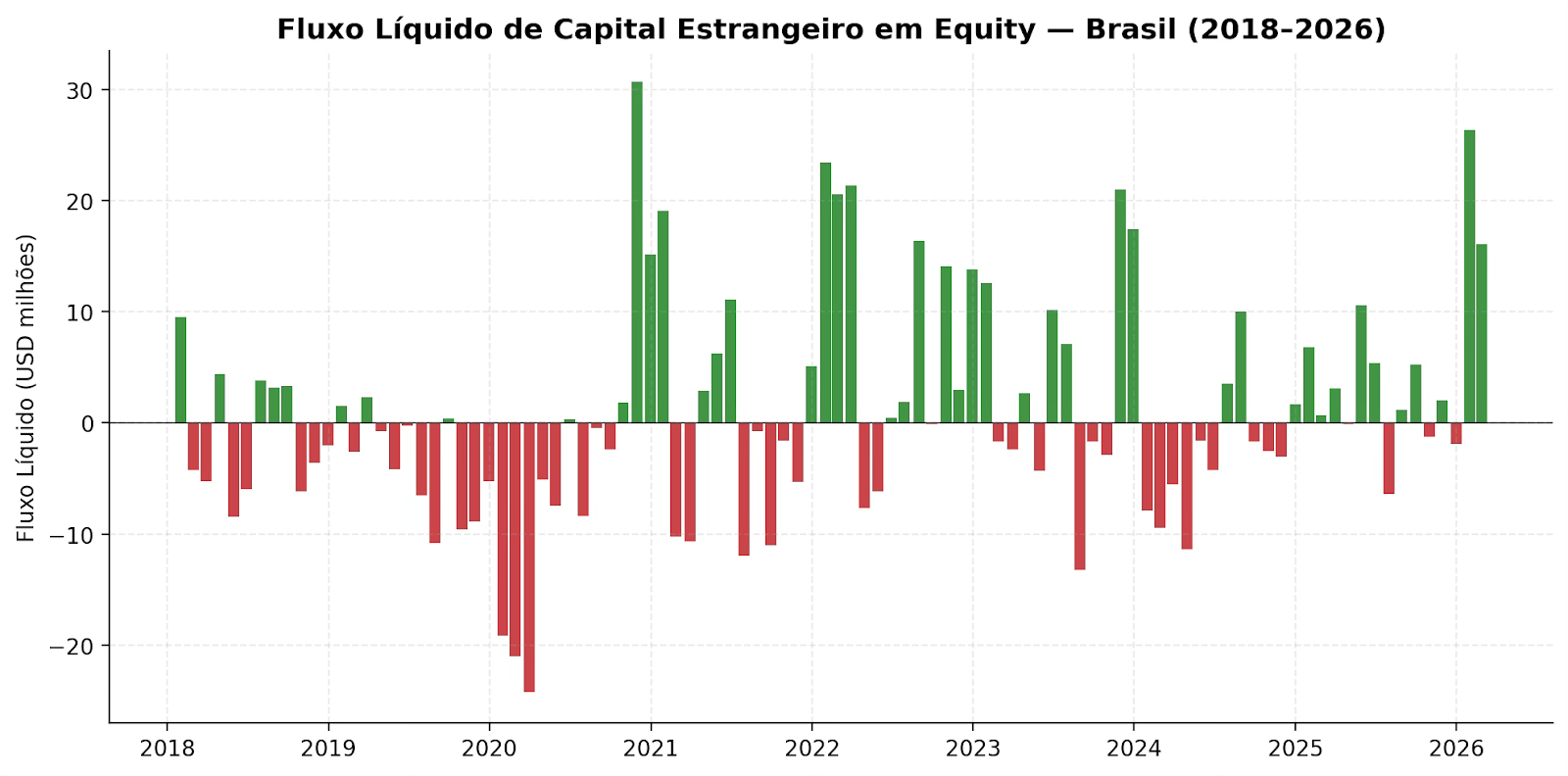

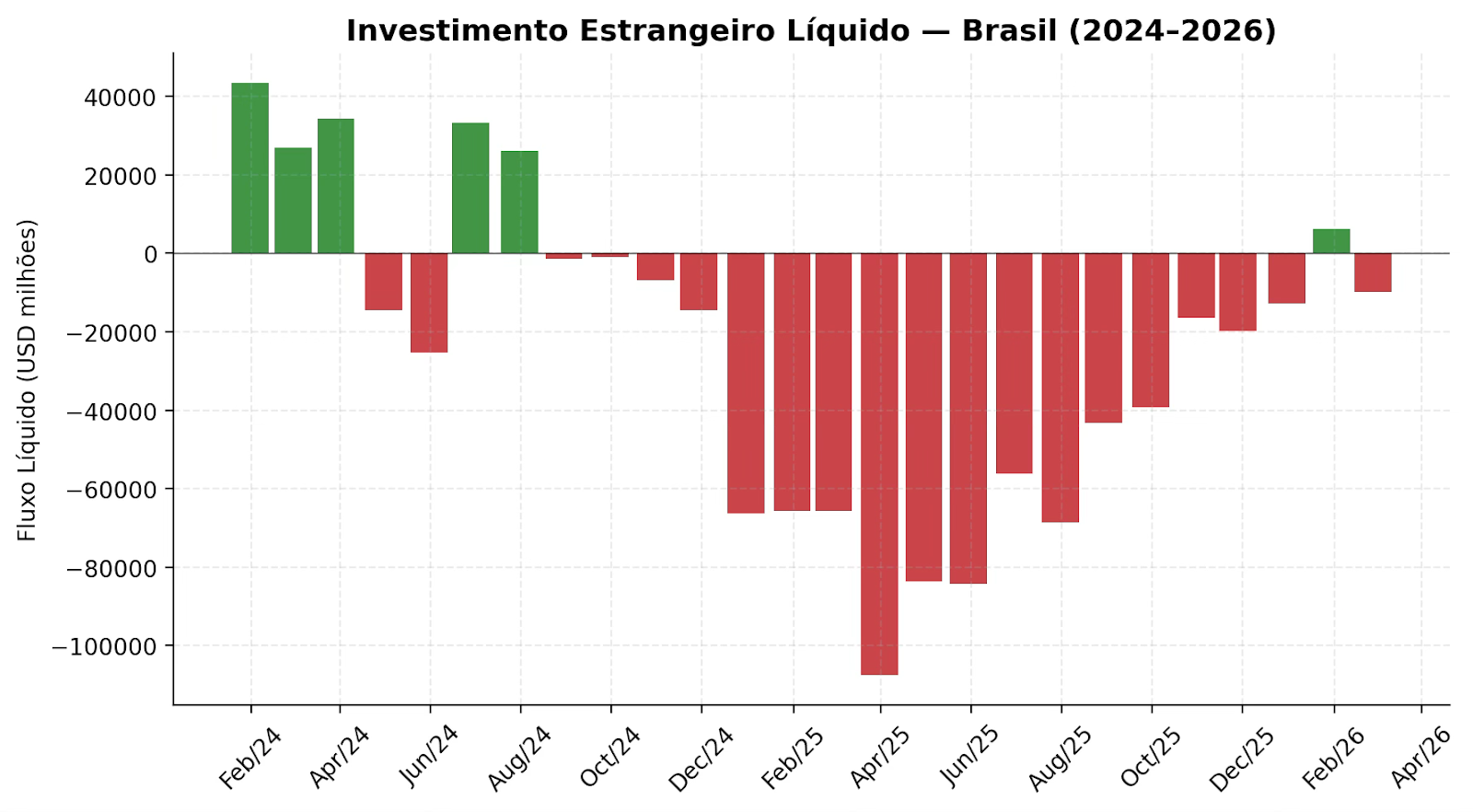

4. The world doesn’t want to keep money here

When you look at foreign investment in the stock market, recent months show inflows. In isolation, it looks positive.

Since 2018, however, the months with capital outflows (red bars) account for 54% of the time. More than half. In 2024, foreign investors pulled R$32.1 billion out of the Brazilian stock market. The Real lost 27% against the dollar. The Central Bank spent $33 billion in reserves in December alone to prop up the currency.

If we zoom out to all Brazilian markets, not just equities, the picture gets worse.

From October 2024 onward, it’s almost all outflows. Red bars dominating the chart month after month. Foreign capital enters occasionally and leaves structurally.

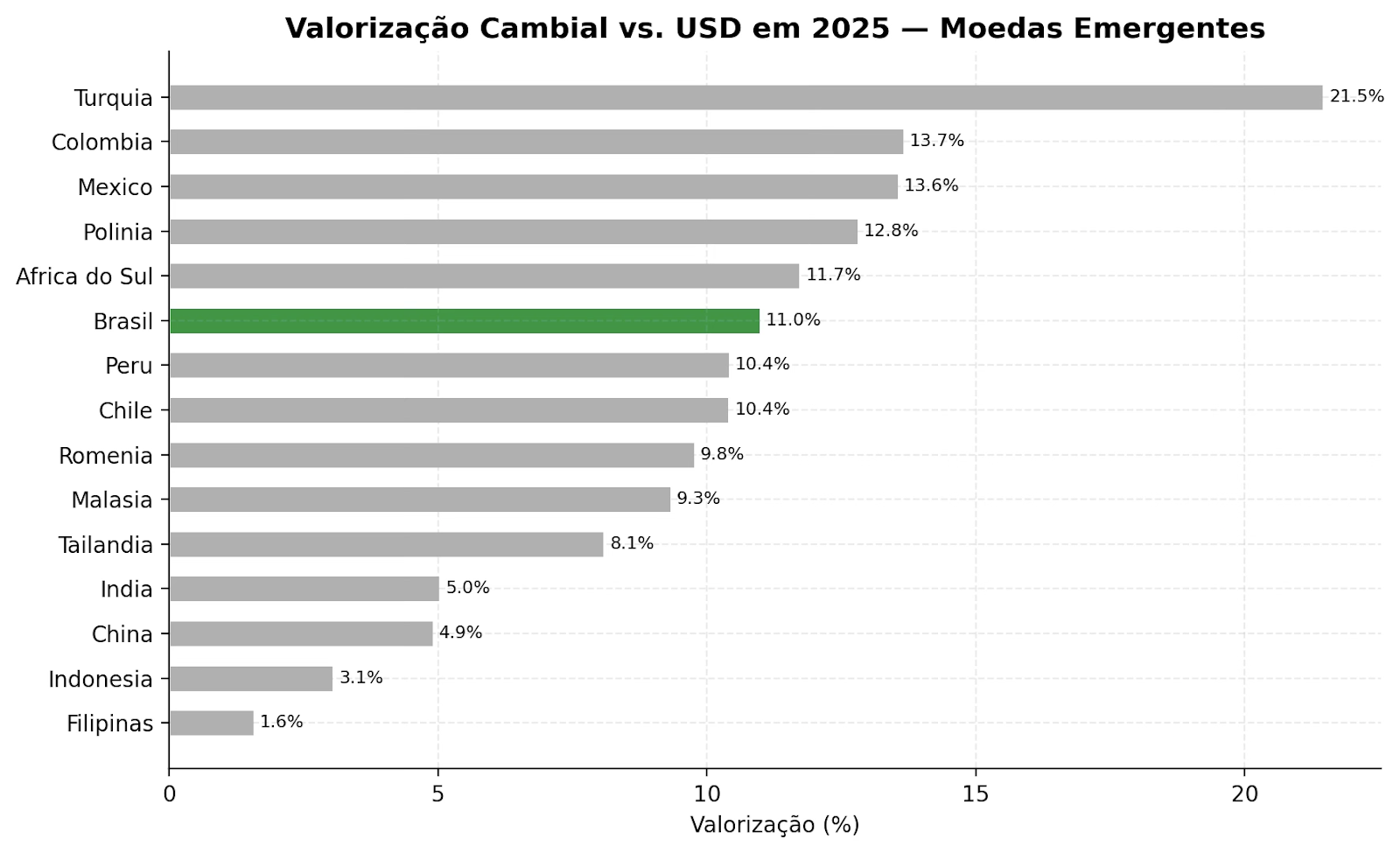

5. The currency underperformed some peers

The Real appreciated 11% against the dollar in 2025. The Colombian peso appreciated 13.7%. The Mexican peso, 13.6%. The Polish zloty, 12.8%. The South African rand, 11.7%.

Brazil shows up in green in the middle of the table, below Turkey, Colombia, Mexico, Poland, and South Africa. And it’s the country that pays the most to keep foreign capital. With the Selic rate near 15%, the cost of attracting investment is enormous, and the result is still worse than countries with much lower rates.

6. The root cause: the fiscal outlook is deteriorating

Everything in the five sections above (low P/E, negative returns, high risk premium, capital flight, weak currency) are symptoms. The cause is fiscal.

The government spends more than it collects. Public debt stands at 87.3% of GDP. Interest payments alone consume R$800 billion per year, or 7.5% of everything the country produces. More than education, healthcare, and infrastructure combined.

To close the gap, the government raised taxes. The new tax system replaces five levies with two, at a combined rate above 28%. The primary balance (the fiscal result before interest) showed a brief improvement from the extra revenue. Some call it the “Haddad effect.”

It didn’t last. The balance is already falling again. When you include interest on the debt, the nominal result shows an accelerating decline.

The tax squeeze is making no difference to the fiscal picture. All the new taxation came through, and the country is worse off than at any point in the last ten years.

The Selic rate at 15% is choking growth. GDP is expected to grow just 1.7% in 2026, while India grows 7.6%. Brazil’s real interest rate sits near 10%, among the highest in the world.

2026 is an election year. With approval ratings falling, the political pressure pushes toward more spending. The Eurasia Group included Brazil in its Top Risks for 2025 and 2026. Capital Economics warned that the election could derail fiscal progress.

The cycle is familiar: the government overspends, the Central Bank raises rates, the economy barely grows, tax revenue falls short, the deficit widens. Each turn makes it worse.

Those with information are leaving

The IFC Review has reported that the tax reform is accelerating wealth migration out of Brazil. Brazilians with more resources and more access to information are moving money abroad. If the people best equipped to analyze the situation are diversifying out, that should serve as a signal for anyone still 100% exposed to Brazilian assets.

What to do about it

If most of your wealth is in Reais (property, business, domestic investments), every data point in this article is a direct risk to your money. More taxes, more inflation, more depreciation. The trend, by the numbers, points to further deterioration.

One of the most accessible ways to protect part of your wealth today is through dollar-pegged stablecoins. You allocate a portion of your capital to a currency pegged to the dollar, earn daily interest, and have 24-hour liquidity. You can withdraw anytime, including nights, holidays, and weekends.

And there’s one feature that changes the entire equation: the money stays under your full control. No bank deposit, no intermediary with access to your assets. Self-custody. Your money, in your wallet.

The government knows this exit exists. The world already uses crypto-dollars for wealth protection.

It’s no coincidence that Brasília is studying tariffs on crypto. If the population understands this mechanism at scale, there will be a run on stablecoins.

Unfortunately, only a very small and privileged slice of the population will realize all of this in time.

Share this article with someone who needs this information.

| A guest post by

|

Really well put article.